Kevin's Weekly Health Tech Reads: The One Medical / Iora Edition

A special edition unpacking the news of Monday's merger between Iora and One Medical

Breaking Down the Iora / One Medical Transaction

Hey y’all - I’ve received a number of folks asking for some perspective on the One Medical / Iora Health acquisition that was announced Monday morning. So if you’ll allow an interruption to your work week, we wanted to share some perspectives on the merger.

One Medical is acquiring Iora Health in an all-stock deal worth roughly $2.1 billion. One Medical will own 73% of the combined entity moving forward, while Iora will own 27%. They’ll now be in 28 markets in total, with Iora in 10 markets and One Medical in 22. The combined organizations will have roughly 636,000 members - 598,000 via One Medical and 38,000 via Iora. In 2021, One Medical expects to generate $475 million of revenue in 2021 and -$10 million of EBITDA, while Iora expects $299 million revenue and -$90 million EBITDA. We’ve included a number of reactions below - here are the links if you want to peruse the merger materials yourself: Link (Investor Presentation). Link (Webcast).

Business Model Diversification

One Medical has always had an opportunistic approach toward business models that drive its next phase of growth, and it appears to have found its next growth story as an organization in value-based care. Remember that One Medical started as a D2C concierge primary care play over a decade ago, subsequently morphed into an employer offering, then added on a health system FFS revenue component, and is now adding a value based care revenue stream. This latest move highlights the allure of capturing the full premium dollar for primary care organizations is apparent. The valuation difference between a FFS commercial primary care member and a value-based Medicare Advantage primary care member is stark - One Medical has roughly 16x the membership of Iora, but is still giving Iora 27% of the combined entity moving forward. Using 2020 revenue and Q1 2021 membership, Iora’s annual revenue per member ($5,605) is nearly ~9x that of One Medical’s annual revenue per member ($635). It makes sense that One Medical would want to move this direction to capture more of the upside associated with value-based models.

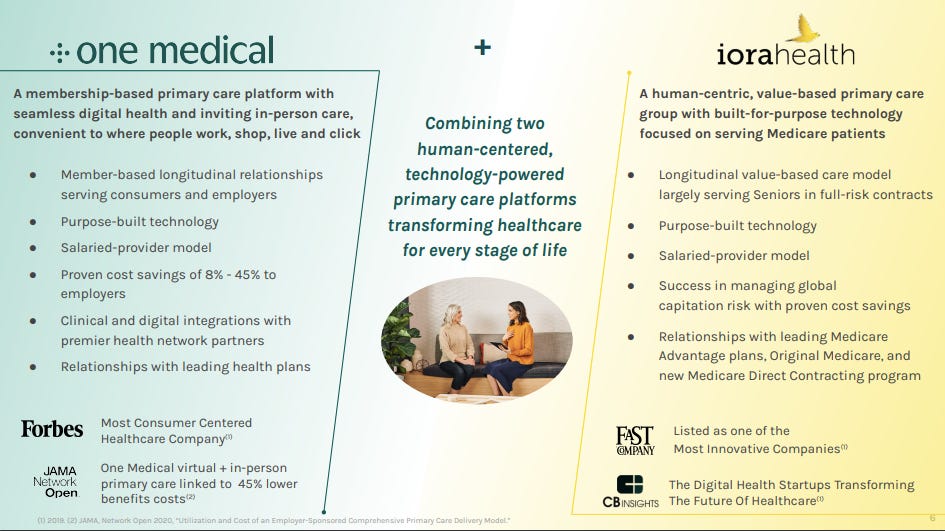

Strategic Rationale

This slide below highlights well the strategic rationale for why the models can and should work well together. Perhaps I’m the only one that notices this or cares, but isn’t it interesting that the only numbers provided on here about “proven cost savings” are from the One Medical side, in the employer market where it’s incredibly challenging to measure savings off a credible baseline? For all we talk about Medicare Advantage primary care models saving money for that population and how value-based care models save money, the lack of solid numbers here speaks volumes - as we can see in their financials (more later) it seems like Iora’s model likely still costs more to deliver.

Direct Contracting

Speaking of the allure of capturing the premium dollar, it’s not surprising to see that the Direct Contracting opportunity is featured repeatedly throughout the investor presentation, as Iora has a Direct Contracting Entity approved in 10 states for the 2021 performance year. Even despite the recent CMS moves to pause on new applicants for the program, it is still a popular growth story for primary care startups. And why not? It’s a massive addressable market opportunity for organizations like Iora to point to. It’ll be interesting to watch what materializes from this program moving forward.

Market Overlap / Synergies

One Medical and Iora expect to see $350 million in revenue synergies from this transaction by 2025, which is quite a large number given their combined estimated revenue in 2021 is only $774 million. These synergies will be driven by the sort activities you’d expect here - One Medical markets expanding into Medicare, Iora markets expanding into commercial, and transitioning One Medical commercial patients to Iora MA patients as they age-in, among other things.

There are lots of questions to answer related to how the organizations integrate the models moving forward across the different consumer types they’re serving. The synergies slides (23 - 24) mentions that they expect to have reciprocal access across various clinics, which makes sense that they will do so. While Iora primarily treats Medicare Advantage patients, as long time Iora observers will remember, Iora has always tinkered with populations outside the Medicare Advantage book of business. Working with commercial populations won’t necessarily be new to them. Iora has struggled growing membership though, and clearly a portion of the synergies baked in here are leveraging One Medical’s consumer centric approach to help Iora grow membership faster moving forward. The age-in opportunity could be massive by itself - assuming One Medical’s membership is evenly distributed among the adult population, they have roughly 12,800 members (600,000 members / 47 years) aging-in to Medicare every year. If they can convert even half of those members to Iora, it’s a massive opportunity for both orgs.

It will be also interesting to watch how One Medical and Iora define customer segments moving forward and how they think about what brand those consumers have a relationship with. Certainly it seems that One Medical will keep focusing on the relatively healthier FFS commercial population and Iora will focus on the relatively sicker Medicare population. Given the different needs of those populations, you could envision a scenario where a combined brand dilutes the tailored approach of each brand. Yet on the investor call, an analyst asked a question about whether Iora’s brand will continue to exist on a standalone basis and the answer wasn’t exactly clear - instead there was a response about creating “the most loved brand in healthcare”. This invites lots of questions around what the handoffs between One Medical and Iora will look like and how these brands will integrate over time.

Platform Integrations

One of the bigger questions in this deal to me is how Iora and One Medical will right-size the investments that each of them have been making in building out their operating models, and specifically their technology platforms. Iora has invested a ton of time and energy into Chirp, and One Medical has rolled out its own virtual visit platform - check out Slide 15 on each organizations’ tech platforms, where each org cites a number of digital touchpoints with members. How will Iora and One Medical migrate everyone to one tech platform? What about operations from a clinical practice perspective? Iora’s whole clinical model was built around a “worry-score” that they assign for each patient with a unique workflow that includes daily huddles with care teams. Are both organizations adopt one clinical model moving forward? You can’t imagine that they do so, but then that makes the tech platform integration significantly more challenging. So you’ve got an issue there. Given the purpose-built nature of these platforms, it seems like a headache to generalize across the two models. It’s understandable that One Medical / Iora haven’t delved into these issues too far publicly, but it seems that these answers will have significant long term impacts on the success of this deal.

FFS vs VBC Incentives

The conflicting incentives between the fee-for-service versus value-based models related to One Medical’s IDN partnership strategy will be something to watch moving forward. One Medical’s business model has relied on partnering with local IDNs and billing employers on a fee-for-service basis via the IDN contract for those visits. Keep in mind that One Medical has been working to be able to tell Wall Street that it has 100% of patients under clinically integrated partnerships with local IDNs, something it has now achieved with an IDN partner in each market they’re in. The IDNs of course benefit by charging for those primary care visits and capturing downstream referral volume. But this is where the incentive challenge comes in, as IDNs are usually a higher priced care delivery option in a local market. Iora, on the other hand, is incentivized to send downstream referral volume to a high quality / low cost provider given it is responsible for managing the cost of care. This probably isn’t the IDN in a local market, so which incentive wins out over time in this organization and how do those IDN partnerships evolve? An analyst asked a question similar to this on the investor call, and the answer wasn’t entirely fulfilling.

And beyond that, what happens when IDNs partner with different orgs across commercial and Medicare primary care markets? If you’re Advocate Aurora in Chicago, it doesn’t seem like you’re too thrilled with this move given you have my commercial business tied up with One Medical and my Medicare Advantage business tied up with Oak Street. One Medical notes that one of the synergy opportunities is to transition members from Commercial to Medicare, which raises some interesting questions as to where consumer loyalty lies with these orgs - is it the IDN or One Medical? Seems like the answer to that question is One Medical. But if One Medical is transitioning those patients away from Advocate’s Oak Street partnership and toward Iora, that is sure to create some tension over time with Advocate.

Iora vs Oak Street

There is of course a natural comparison to make here between Oak Street and Iora. Obviously Oak Street’s current valuation of just shy of $15 billion is markedly higher than Iora’s acquisition price of $2.1 billion. If we had to guess at the reasoning between Oak Street’s and Iora’s difference of valuation, a lot of it would come down to how they’ve been able to 1. grow membership and 2. manage risk. Oak Street is roughly double the size of Iora today - in terms of markets (20 vs 10) and number of clinics (86 vs 47), and over 4x the number of total at-risk members (75,500 vs 22,800). But this doesn’t explain the massive valuation difference between the two - Oak Street is currently trading at an Enterprise Value around $14.6 billion while Iora was acquired for $2.1 billion. This implies Oak Street is being valued at ~$193,642 per at-risk member while Iora is being valued at $92,105 per at-risk member.

It seems that Iora’s struggles with medical cost management is behind at least some of that valuation gap. In 2020, Iora was at a -16% Care Margin (revenue less medical claims paid less direct cost of care), while Oak Street generated a 9% Platform Contribution margin. While that’s not quite apples to apples comparison - it appears Iora includes its original Medicare FFS business in it - it seems directionally accurate. It appears Oak is performing better both in terms of managing medical claims paid (74% of revenue versus 86% of revenue), and in managing their direct costs of operating their primary care model (18% of revenue versus 31%). It’s problematic that Iora’s margins still look like this after years of operating this model - you’d hope its financials would look better by now. Iora / One Medical is setting a long term target of 17% EBITDA margin, which will require significant financial improvement over time.

The Takeaway

Whatever way you cut this, this is a big deal in the primary care innovation landscape. One Medical and Iora now have a joint primary care offering that spans the lifetime of its members - from pediatrics to adults to seniors.

The combined organization sets itself up to capitalize on a number of potential future growth opportunities and ensure its ongoing relevance in a rapidly evolving space. Between One Medical’s relationships with employers and IDNs and Iora’s relationships with health plans, the combined organization is entrenched with key players across the healthcare landscape. On top of that, One Medical gets to diversify away from its fee-for-service revenue stream, while Iora finds a partner for its next phase of growth. This makes strategic sense for both parties.

The differences in underlying strategy and culture related to the fee-for-service model and the value-based model seem destined to create some friction between the two orgs that will be worth watching over time - which set of incentives will win out when push comes to shove? Both organizations have invested heavily to create purpose-built platforms to support their specific care models, and integrating those two platforms (technologies, operations, clinical models, cultures) seems as though it will be a complicated journey. It’ll be interesting to see whether 5 years from now this organization looks more like Iora or more like One Medical - either way it’ll be a fun transformation to watch as an outsider.