Kevin's Weekly Health Tech Reads 6/6

Babylon Health's SPAC, VC market maps of the women's health and pediatrics startup landscapes, ant more!

The Babylon SPAC:

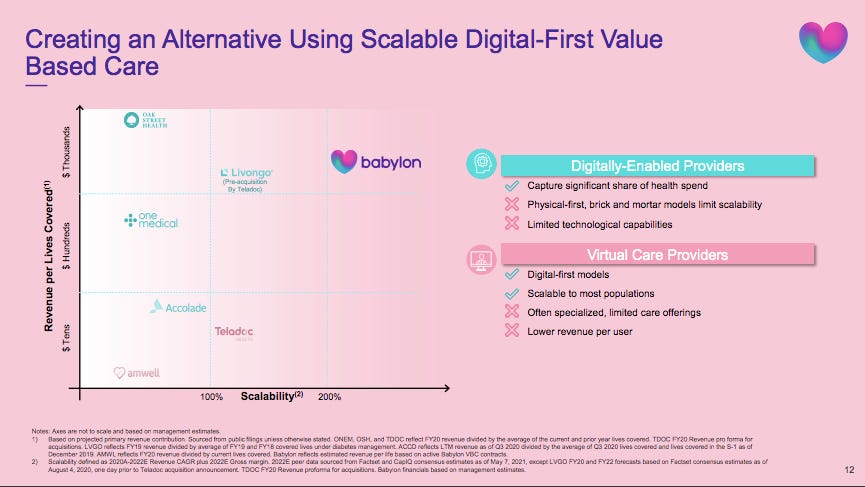

Babylon announced its SPAC this week for $4.2 billion and is another example of a company branching out into new lines of business as it is going public. Babylon is expanding from an AI-based chat service for primary care clinics to a company taking global risk for populations of patients leveraging both digital care and clinics it has acquired. You can see in the competitive landscape slide below that Babylon is trying to pitch itself as the best of two worlds in digital health: the scalability of digital solutions (the x-axis) with the revenue capture of value-based care solutions (the y-axis). Like any investor presentation, Babylon sees itself as all alone in the upper right quadrant. Link (Investor Presentation).

Some additional notes on Babylon:

Babylon got its start years ago as an AI-chat based primary care service wrapped around a primary care clinic in England. It was a bumpy ride at times in England, as Babylon encountered substantial resistance from other clinicians, but it has successfully grown to be one of the largest practices in England (this Wired article is a good summary of the journey). The two primary complaints about Babylon are interesting to explore: 1. the product is bad; and 2. it’s screwing up how they get paid (see Wired article). As a consumer of healthcare, I’m significantly more concerned about #1 than #2.

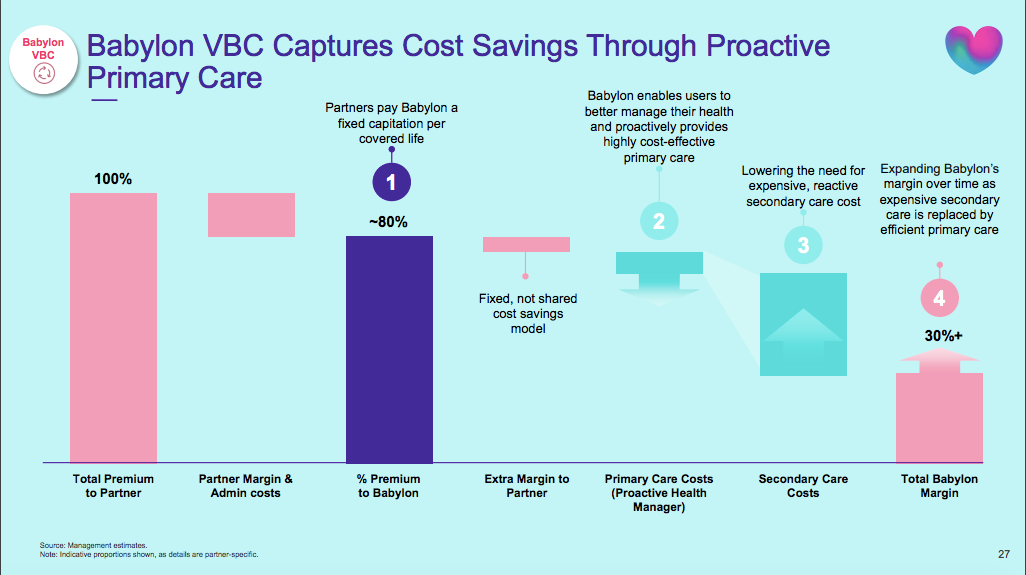

The main story of the SPAC is about how the AI chatbot is just an entree for Babylon to manage delegated risk through its virtual-first primary care model. Check out this slide depicting how it intends to make money in a value-based care environment. This is a pretty straightforward model for a value-based care primary care entity (i.e. see Oak Street’s Investor Presentation which contains basically the exact same chart).

Steps 2 and 3 on this chart get to the whole crux of how many primary care models claim to manage overall spend and will ultimately determine if Babylon is successful or not. The traditional theory of the case is that you *increase* primary care spending in order to avoid downstream costs. Hire care teams, encourage people to come in for more visits, etc. But Babylon appears to be saying it both intends to reduce primary care costs via it’s more efficient model (#2) as well as decrease specialty costs at the same time (#3). While it seems plausible that this could be the case, the SPAC presentation is light on details supporting that Babylon has done this at scale.

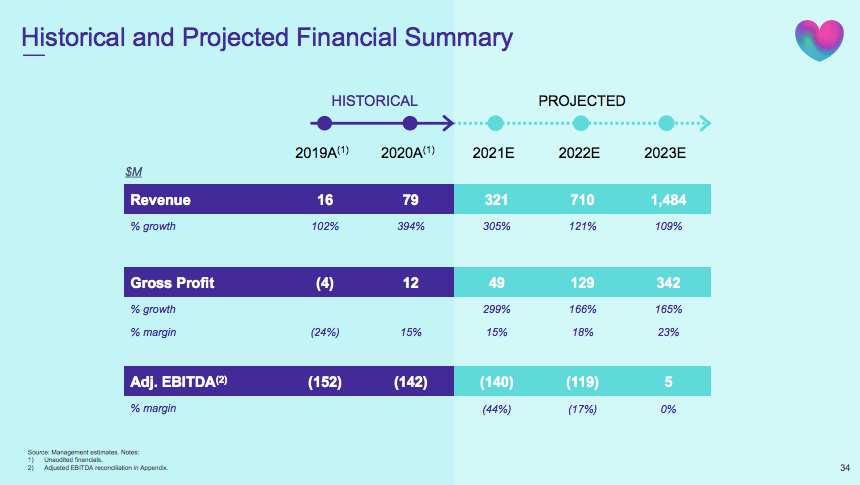

This growth in value based care seems to be driving a significant improvement in financials for Babylon, which is core to the story here. There’s little discussion of the historical financials, but this chart below shows that Babylon’s EBITDA was negative $152 million and $142 million in 2019 and 2020. It expects to lose another $140 million in 2021, before hitting breakeven in 2023. Note this is expected to happen during a period of hyper-growth for the company, as it expects to grow revenue from $79 million in 2020 to $1,484 billion in 2023.

The growth in both revenue and EBITDA appears to be largely driven by value-based care contracts, as it depicts below in slide 26. This is an interesting slide demonstrating why Babylon is migrating to VBC contracts - it can generate thousands of dollars per member per year at margins above 30% in year 3. Reading the footnotes on this slide, it appears that estimate is based off competitors results, rather than Babylon’s experience in the space, again highlighting how much of this model is theoretical at this point. But, the slide certainly depicts the lure of value-based care models quite well for any digital care organization. You can capture significantly more revenue per life covered, and potentially generate really nice margins if you can manage the total cost of care well. Will be worth watching whether Babylon can turn this into reality.

As mentioned earlier, the SPAC deck doesn’t give a lot of detail supporting the notion that Babylon can actually manage medical spend. It glosses over the fact that a key driver of Babylon’s value-based care growth in the US has come from two provider acquisitions in California (First Choice Medical Group and Meritage Medical Network). The strategy of acquiring existing providers only gets a vague mention in Slide 36 that Babylon has an “opportunity to consolidate brick & mortar, integrated care providers in the US”. Note that Babylon currently has 90k capitated lives in the US, roughly 52k of those coming from California, which appears to be from those provider group acquisitions. It will be interesting to see how Babylon performs in these contracts over time - it acquired First Choice Medical Group from agilon health, which was forced to jettison its California business pre-IPO because it was performing so poorly financially. First Choice has 50k lives in Medicare Advantage and Medi-Cal plans. While Bright seems to have provided a proof point that companies can go down this path and successfully manage medical spend, it’s not clear from this deck why Babylon will have any better luck than agilon health did in managing costs. Seems like there is some significant risk in that for Babylon.

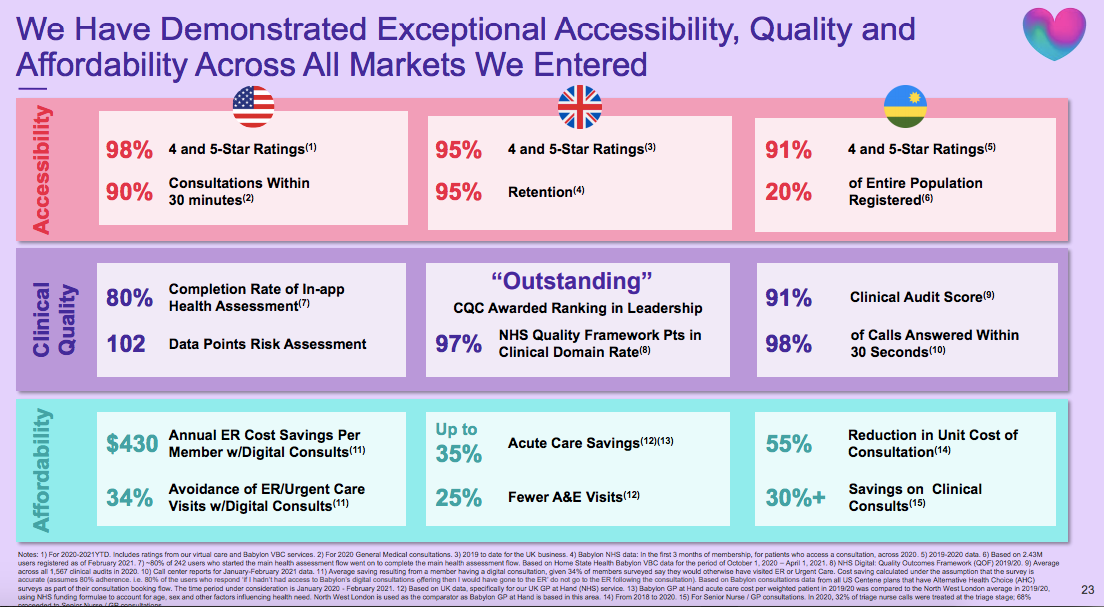

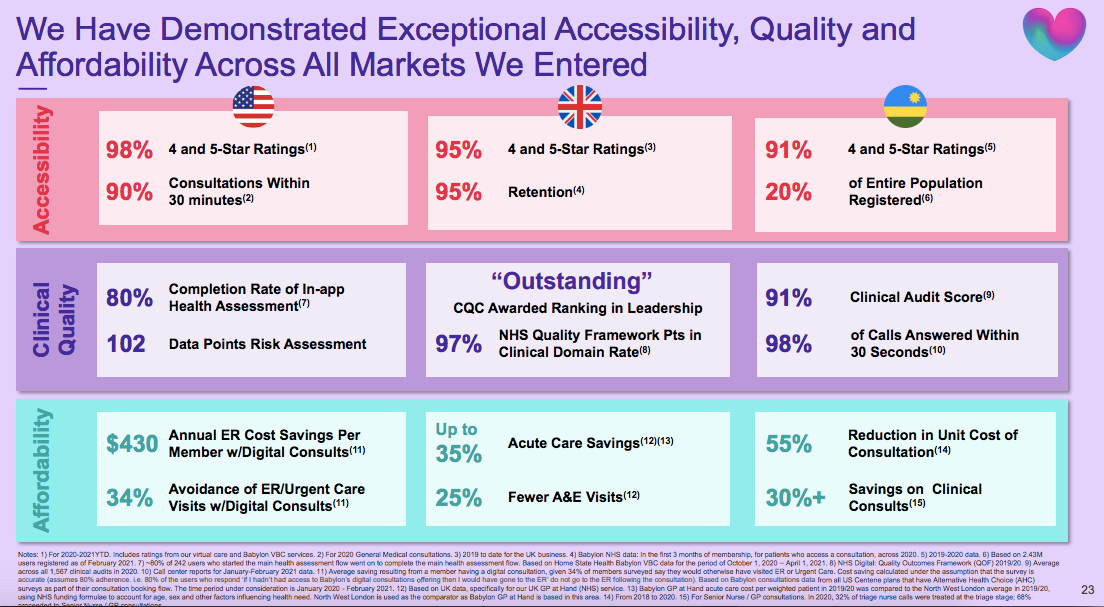

I’m not really sure what to do with Babylon’s key metrics slide. It seems to inadvertently highlight the hodgepodge approach - note the different metrics chosen across different geographies. For example, in the US, Babylon highlights that 90% of consults are within 30 minutes, but that data is not shared for either of the geographies. If that’s a KPI for accessibility, why not share across all geographies? The way they’re calculating savings on the affordability section based on the footnotes also seems a bit… generous? I’m also confused by the US affordability number - are they just stating the same thing two different ways? It’s understandable for where Babylon is at given its recent growth, but you’d hope to see some more consistent KPIs here.

Babylon tucked into this news that it has exercised its option to acquire the remainder of health kiosk startup Higi, which it presumably received when it led Higi’s most recent $30 million funding round.

Some Concluding Thoughts:

Babylon is going to be a very interesting experiment to watch on the public markets over the coming years. I’d love to see it more credibly talk about how it plans to manage risk successfully - I’m not convinced from the SPAC presentation that they know how to do this yet. The approach Babylon is taking is certainly unique in terms of leveraging a digital platform (+ acquired practices) to manage risk, and if they’re able to do this successfully there is a lot of opportunity for Babylon moving forward. Again, that seems like the crux of the case here - if you believe they can do that successfully, this should be a home run.

I’ll be keeping an eye on what their first few quarters as a public company look like, as it seems like there is a lot more to unpack in this one beyond the SPAC presentation. Like many SPAC presentations, it leaves a lot to be desired for folks who want to understand what Babylon has proven out over the last few years versus the shiny growth story. I’m quite skeptical of how they’re going to get to profitability in 2023 - it would be nice to see more details on the financials behind that (as well as historical financials).

Right now, Babylon seems like a nice story with a lot of promise that hasn’t been proven out yet and has some major question marks yet to be answered on the operational side of things.

How do you feel about Babylon? What do you agree / disagree with above? Let us know if you’re bullish or bearish on Babylon’s approach and why you feel that way via this survey. We’ll again post results / interesting comments we hear back from folks.

News:

Blackstone, Carlyle, and Hellman & Friedman are acquiring a majority interest in Medline, a family-owned manufacturer and distributor of medical supplies that did $17.5 billion in revenue in 2020. Link.

Cerner is rumored to be the target of an acquisition. Who knows if this materializes into anything real, but it is fun to think about as the four players mentioned would each be quite interesting: Microsoft, Google, Oracle, and Salesforce. Link.

Children’s Hospital Colorado last week declared a mental health state of emergency as suicide attempts / ER visits related to mental health crises were up 90% last month. This is a heartbreaking article to read about how our health system is failing kids. Link.

North Carolina health systems Sentara and Cone decide not to join forces. Link.

Funding:

D2C telemedicine startup Thirty Madison raised $100 million in part to take its D2C approach to health plans. Thirty Madison, which got its start similar to Ro and Hims targeting hair loss, among other things, is now aiming to expand in chronic care spaces such as diabetes and heart disease. The pitch to payors and employers is presumably as a hybrid that offers a consumer-oriented brand to treat basic conditions while while also managing higher cost conditions competing with the likes of Livongo, Virta, and others. It’s a lot to tackle but will be a cool test. It will be interesting to watch players in the D2C space like Thirty Madison start to attempt to capture value via B2B2C sales, which is an entirely differently animal. Does the consumer-first lens provide a leg up in the race to build digital health platforms? We’ll see. Link.

Nayya raised $37 million for its employee benefits platform. Link.

Aunt Bertha, a network of social determinants of health resources, raised $27 million. Link.

Plum, a startup building an employer insurance offering in India, raised $15.6 million from Tiger Global. Link.

Axle Health, an API layer connecting virtual care delivery startups with clinicians to do in-person home health visits, raised seed funding. Link.

Opinions:

The Substack Health Tech Writers Guild put out some good content this week:

Christina Farr and crew did a deep dive on the women’s health market - I particularly like the market map they put together as a framework for thinking about how broad this space is. The post offers up some good thinking around the women’s health landscape, why it is so relatively underfunded compared to the rest of healthcare, and opportunities moving forward. Link.

Olivia Webb follows up her piece on Direct Contracting and takes a look at capitated models in primary care more broadly. Link.

Kevin Wang dives deep into patient reported outcome performance measures (PRO-PMs). If you’re interested in what PROs are, how they can be used as performance measures, and how they’re collected its worth checking out. Link.

7wireVentures shared a report on pediatric health with a nice market map on the current state of pediatric health startups and some of their predictions for the space. Link.

This is a excellent read in the New Yorker on how Hahnemann Hospital in Philadelphia shut down after a PE firm purchased it from Tenet. As more and more healthcare delivery in this country becomes backed by PE / VC money, it is going to be worth keeping an eye on the side effects of this trend. Link.

Here’s an interesting piece from STAT on why machine learning is struggling in healthcare, looking at how AI models are challenged because the underlying data in healthcare is awful. Link.

Speaking of sketchy AI algorithms, this FastCo article looks at how Epic deployed an AI algorithm for patient triage in hospitals during the COVID-19 pandemic. Link.

Jobs:

Allara Health, a startup building a chronic care platform for women's health, is hiring a Senior Software Engineer. Link.

Cityblock Health, a primary care startup for Duals populations, is hiring a Senior Business Intelligence Analyst and an Analytics Engineer. Link 1. Link 2.

Ginger, an on-demand mental health startup, is hiring a Product Manager. Link.

Ribbon Health, a healthcare data platform startup, is hiring a Provider Performance Product Manager. Link.

Thirty Madison, a D2C telemedicine company, is hiring a VP of Payor Strategy & Business Development. Link.