Kevin's Weekly Health Tech Reads 6/20

Cano Health makes an acquisition, RIP Medical Debt eliminates $278m of patient bills, and more!

News

Cano Health, the recently SPAC-ed Medicare Advantage primary care provider, is acquiring University Health for $600 million. University is another MA primary care provider in South Florida, with 13 clinics and 24,000 Medicare Advantage members. Link.

On the public markets, two IPO valuation updates:

Bright Health is targeting a valuation of over $14 billion at its upcoming IPO. It is wild when you compare that to Oscar at just under $5 billion. Sure seems like we’re going to see a lot more of Bright’s growth via acquisition strategy over the next few years. Link.

Doximity is targeting a valuation of ~$4B. Link.

In some uplifting news, RIP Medical Debt is buying and eliminating $278M in patient hospital bills for 82,000 low-income patients from Ballad Health, a large health system in Virginia and Tennessee. What is striking is that many of these people should never have received bills to begin with because of financial aid programs that exist. But because those people don’t know they are eligible and/or it’s hard to apply, they can’t take advantage of the programs. With all the crazy valuations out there, seems like there is a significant opportunity just to make it easier for people to find and enroll in the programs that exist to help ease the financial burden of care. Kudos to RIP Medical Debt. Link.

Humana acquired Florida-based home health provider Onehome. Link.

Health insurance startup Sana has opened a primary care clinic in Austin in partnership with Proactive MD. Link.

Michigan-based health systems Beaumont Health and Spectrum are planning to merge. Link.

Funding:

Mental health startup Lyra Health formally announced it raised $200 million at a valuation of $4.6 billion. Link.

Brightline raised $72 million as the behavioral health for kids market continues to be a very attractive space for venture dollars. Brightline is currently in two states (Massachusetts and California), but plans to be in all 50 states by the end of the year. Link.

Jonathan Bush’s new effort Zus Health made waves this week, announcing a $34 million round from Andreessen and others. Zus launched with an interesting set of health care delivery disruptors as customers - Oak Street, Cityblock, Firefly Health, and Dorsata. From a strategic perspective, you can see why there’s a lot of excitement around this idea as it fits very neatly into the thesis that new infrastructure platforms will emerge to enable new care delivery models. There are a lot of big names associated with it and it is launching with some big customer names in startup land. All signs seem to point to it being a good idea coming along at the right moment in time as digital-first care models ramp up. It’ll certainly be worth watching what adoption of the Zus platform looks like over the coming months / years. Link.

A handful of interesting questions in here:

If the back-end of “tech-enabled care delivery” startups can be abstracted away to a single platform like Zus, how much of the proprietary tech that the care delivery models have developed - and drives so much of the valuations - is actually that unique? A couple of years from now I could see platforms like Zus deflating valuations in the care delivery market as more folks realize many of these companies are functionally just provider orgs that maybe have a unique contracting strategy. Not that that’s a bad thing - and it’s probably a good thing for Zus - it just seems that there’s perhaps too large of a valuation gap between the VC-backed care delivery models and the local provider group.

How long until these new care models Zus is targeting have a meaningful portion of the population in the US under management? Between Oak Street (~100k members) and Cityblock (~70k members), Zus has around 170k patients. So round up and say in total that’s 200k patients. For perspective, that’s probably less than half of the patients that the regional health system in the closes metro area to you serves each year. And Oak and Cityblock are two of the biggest new care delivery players out there! So it seems like a big bet that that number of patients attributed to new care delivery entities will dramatically accelerate over the next few years. Either that or you see Zus start working with more incumbent providers as well (which seems like it would be quite smart on their part).

What will be the competitive reaction of different care delivery companies playing together on this platform? I am particularly curious about how the virtual primary care companies will react to Bush’s dabbling as both the platform (via Zus) and the care delivery company (via Firefly Health, where he is Exec Chair). If I’m Galileo, Amazon Care, or others in this market, I’d have a lot of questions about the competitive dynamics at hand with Bush playing both roles.

The Pill Club, an app that allows people to mail-order birth control, raised $41.9 million. Link.

Stork Club, a startup helping navigate people through fertility journeys, raised $30 million. I love the concept here and these sorts of solutions are desperately needed in the fertility space. I do wonder about the business model a bit though - Stork Club is focusing on selling the service to employers as a way to reduce healthcare spend by preventing million dollar babies. Of course employers seem to be excited by it, evidenced by Stork Club’s 5x revenue growth last year. But what does Stork Club do when employer interests diverge from user interests? Link.

Sempre Health, a startup working on reducing out-of-pocket costs for medications, raised $15 million. Link.

Form Health, a startup building a telehealth model for obesity, raised $12 million. Link.

Uplift raised $3.1 million to help people find in-network therapists. Link.

Ksana raised $2 million to build a platform that passively collects phone data to measure mental health. Link.

Opinions:

MedPAC continues to pick a fight with all your favorite Medicare Advantage payors as it again suggests Medicare Advantage actually increases costs versus Medicare FFS programs, this time in its June 2021 report to Congress. It recommended that CMS adjust Medicare Advantage benchmarks as a way to reduce costs. It also suggested streamlining alternative payment models. The drumbeat continues to get louder on that front. Link (Summary). Link (Report).

Apple was featured this week as the latest tech giant struggling in its quest to disrupt healthcare. A WSJ article suggests that its decision to takeover its primary care clinics from Crossover Health a few years back hasn’t quite worked out as originally planned. Turns out scaling primary care clinic models is hard? Shocking. Link.

Google was also in the news with a reorg of the Google Health team in what appears to be a blend of struggling to show progress in the consumer health side of things and realizing the need, and opportunity, to refocus efforts on platform businesses in healthcare. The team reassigned about 20% of employees to other groups within Google and restructured Health into 3 groups: 1) Care Studio - platform allowing to providers to “essentially perform Google searches on patients’ EHRs, 2) Health AI - software tools to aid is screening and diagnosis; 3) Clinical and regulatory focused team. The consumer health team (health devices and apps) also appears to be no longer with most of those employees reassigned to Fitbit team in the Devices and Services group. The move makes sense for Google to focus on doing what it does well in setting up the infrastructure and platforms for companies (in this case providers) to do what they do well. The question then becomes will Google ever know healthcare well enough to do that better than other companies closer to the healthcare market. Say like… Zus? I’m skeptical, but we’ll see… Link.

This is a super interesting article in Time looking at mental telehealth and disparities in telehealth adoption. Link.

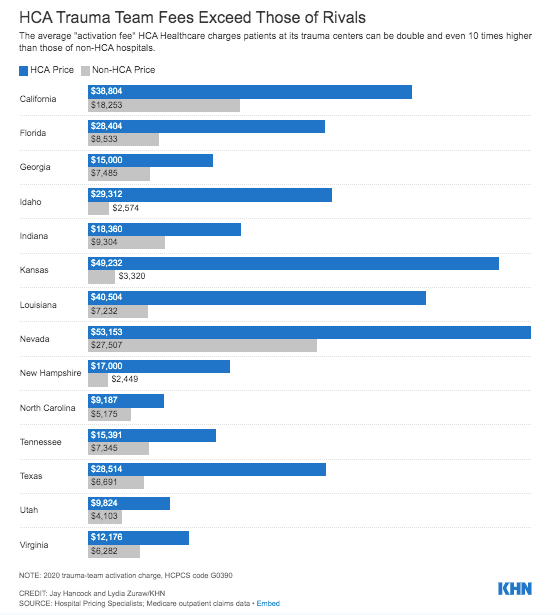

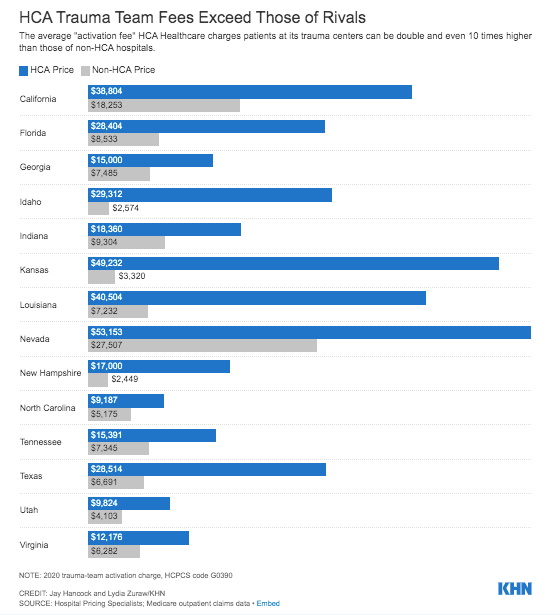

KHN shared a really in depth report on HCA’s use of trauma centers and how it makes a pretty penny of trauma centers. Reports like these highlight the challenging mix of incentives in for-profit healthcare. Are more trauma centers helpful for patients? Probably yes (although the article makes a good point about multiple trauma centers in one city). Is HCA profiting nicely off this strategy? Probably yes - look at the chart below of what HCA is charging versus other trauma centers. Most are more than twice as high as non-HCA hospitals. Does this increase healthcare costs in this country? Probably yes. Do HCA shareholders benefit? Uhhhh… yes. Link.

Data:

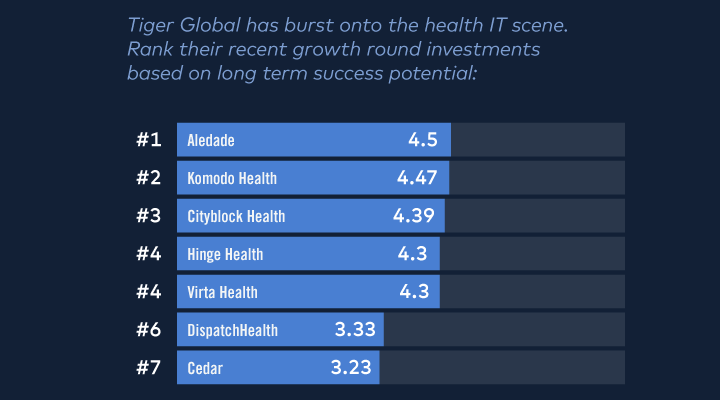

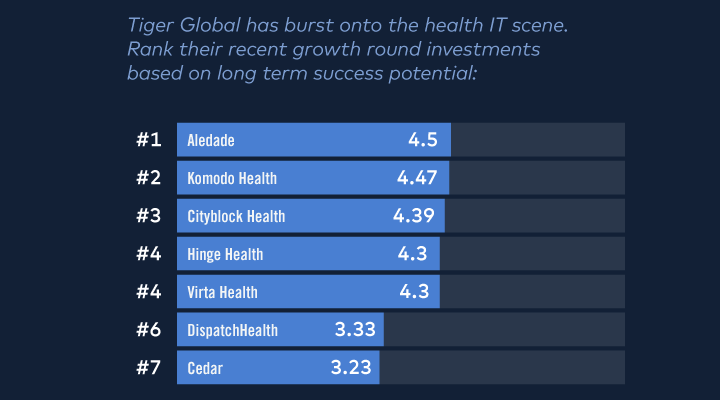

Venrock released its survey on healthcare leaders sentiments towards the space. There’s a number of questions / answers in here worth checking out. Perhaps the most interesting was this question looking at Tiger’s most recent investments by their long term success potential - Aledade was first, followed by Komodo and Cityblock. Dispatch Health and Cedar are notably lower than the others. Link.

This is a good piece from Axios looking at predatory billing practice of hospitals. Interesting to see the data that ten hospitals in this country are responsible for 97% of lawsuits against patients. Link.

Jobs:

Amino, a startup helping employees find / navigate care, is hiring a data analyst and a data scientist. Link. Link.

Commure, provider workflow platform startup, is hiring an Accessibility Designer. Link.

Conceive, a startup building a community and resources for women's health focused currently on fertility, is hiring a Founding Engineer. Link.

ICANotes, a behavioral health EMR+PM company, is hiring a Product Manager. Link.

ixLayer, an end to end software platform for precision health testing startup, is hiring a Senior Product Marketing Manager. Link.

Meru Health, an online mental health provider startup, is hiring an SVP of Ops, a RVP of Sales (Western) and a CFO. Link 1. Link 2. Link 3.

Truepill, an API-connected healthcare infrastructure startup, is hiring for various Strategic Finance roles. Link.

Vim, a digital infrastructure startup connecting data and provider workflows, is hiring a Product Marketing Manager. Link.

Zus Health, a startup focused on building a platform of healthcare-oriented, API-first services, is hiring a UX Research and Design Lead. Link.