Kevin's Weekly Health Tech Reads 2/7

This is a long one: Oscar's S-1; SPAC news (Clover, 23andMe, Talkspace); lots of VC funding rounds; another insane read on hospital billing, and lots more!!

Reads for the week of 1/31 - 2/6

The Oscar S-1:

Oscar filed its S-1 on Friday! The S-1 itself is pretty high level and a bit shorter on some details than I would have hoped for. For instance, it’d be great to have financials prior to 2019, or some detail on how their partnerships are performing. But alas, some takeaways from the S-1 are below. Link (S-1).

The basics: Oscar currently operates in 18 states, having expanded to 15 of those states since 2017. Oscar offers insurance plans for the Individual, Small Group, and Medicare Advantage markets. It says it is the third largest for-profit insurer in the US for the individual market. Their biggest membership states include Florida (115k members), Texas (104k members), and California (93k members). Interestingly, New York (where Oscar got its start) saw a large decline in members this year from 51k to 39k. Pg. 73.

The annual Oscar tradition of lighting piles of money on fire each year as a tribute to their membership growth deity is readily apparent in the financials. Oscar has accumulated a $1.4 billion deficit over the years, and it lost $261 million in 2019 and $407 million in 2020. That is a whole lot of money to burn through eight years in since it was founded in 2012. Pg. 23.

Membership does continue to grow quite nicely in the individual and small group products - growing from 230k members in 2019 to 400k in 2020 (and they’re currently at 529k total members as of 1/31/2021). 2020 was Oscar’s first year in the Medicare Advantage market, with only at 1,924 lives there - another reminder of how hard it is to grow in that space. More on that in a bit. Pg. 73.

On the other numbers… Premium revenue grew to $1.7 billion in 2020, up from $1.0 billion in 2019, both after risk adjustment and corridors. Oscar’s net revenue actually went down, from $488 million to $463 million due to their reinsurance agreements. Oscar ceded 55% of its premiums in 2019 and 77% in 2020 to reinsurers. MLR went from 87.6% in 2019 to 84.7% in 2020, which Oscar attributes in part to COVID-19. Admin expenses actually went up from 25.5% in 2019 to 26.1% in 2020, but it looks like it was driven by an increase in ceding commissions, which as I understand it is a fee paid to the reinsurers. If you exclude that, admin expenses went down from 19% in 2019 to 18% in 2020. Either way, that number will need to drop over time if Oscar’s going to get to profitability. Pg. 18, 38, 71, F-18.

Oscar lists out five potential opportunities for growth: 1. acquire more members in existing markets; 2. launch new markets; 3. create new products; 4. new partnerships / acquisitions; and 5. monetize the platform. 1 - 3 seem pretty straight forward, I’m most interested in 4 & 5… more below. Pg. 119, 120.

Not surprisingly, Oscar’s platform play makes a big appearance throughout the S-1 as a core part of the growth story. They cite their partnerships with Cigna, Montefiore, Cleveland Clinic, and Health First a number of times in the document as examples of how their platform can be leveraged. The document is light on details for these relationships, but they do reference they can monetize them either through risk-sharing partnerships or fee-based service arrangements. It appears that Health First is the first fee-based service arrangement Oscar has in place. It’s worth noting the adjacent markets they list that the platform could go after - telemedicine, care concierge, claims management and population health. Pg. 4, 120.

Oscar plays up its virtual platform and member engagement as a key source of differentiation versus other insurance offering. Here are some of the more interesting stats they shared (note that most of these stats are for subscribing members, which is the one member who subscribes - i.e. not their dependents):

47% of members over 18 years old and 44% over 55 years old are monthly active users. 81% over 18 and 75% over 55 have created a digital profile with Oscar. Pg. 118.

71% of members and 90% members with a chronic condition have used their Oscar Care Team. Pg. 111.

37% of members who have had a visit with any provider have used Oscar’s virtual visit platform in 2020 (I’d be curious what that number would go to if it were just all Oscar members). Pg. 103.

In 2019, 19% of Oscar's members total visits to PCP, urgent care, and EDs were to Oscar’s virtual visits (note this is pre-COVID too. But wait, why not share the 2020 data? I assume that went up a lot?) Pg. 103.

46% of first-time visits to major specialties were driven via the Oscar app or care team, resulting in a median member savings of 7% in 2020. Would be interesting to see how this compares to a non-COVID period. Pg. 103.

Oscar launched a virtual primary care offering January 2021. It will be curious to watch how that impacts the engagement metrics above over time - hopefully this is something that they’ll report on. Pg. 113.

It’s interesting in the context of all of the virtual engagement talk that Oscar Medical Group, which appears to be the provider entity that staffs Oscar’s virtual visit platform, does not play a very prominent role in the S-1. It’s largely only discussed as a risk factor to the business if Oscar loses the contract and no longer can support virtual visits. You could envision this entity as a central growth element of Oscar’s story, particularly with the launch of the virtual primary care offering, but it doesn’t appear to be the case, at least based on this document. Seems like this would indicate we’ll continue to see more provider partnerships for Oscar. Page 35.

This chart on Oscar NPS is interesting in that it’s the exact opposite narrative I would have expected - the highest NPS age groups are 55+. And their 55 - 64 age group is also their highest percentage of membership at 20.9%. Their lowest NPS is with the millennial crowd, 27 - 35. But then it’s higher in the 18 - 26 group. Curious. Pg. 117 - 118.

As an aside, this has to be a core part of Oscar’s MA growth strategy, right? You take that 56 - 64 age group, which is the largest group (at 21% of their membership it’d be about 110k members in that category, or about 12k members who are 64 years old) and when they turn 65, Oscar could flip all of them into an MA plan? Seems like they’re in a good position to do so. Will be very interesting to watch this over the next few years.

I’m not sure why, but it doesn’t appear Oscar included a competition section in the S-1. I would have been quite interested to see who they listed as their competitors. Yet again, a little disappointed by this S-1.

Almost 30% of Oscar’s medical claims were paid to three provider orgs - AdventHealth (11% of medical), Tenet (9%), and HCA (7%). This is perhaps not surprising given Oscar’s largest membership is in Florida, Texas, and California. But it is interesting to see Advent at the top of the list. Pg. 36.

To summarize, there seems to be a pretty clear bull and bear case for Oscar:

Bull: They’ve built a differentiated technology chassis enabling a better insurance experience. They’ve already demonstrated the platform is of interest to others - i.e. Cigna, Health First, Cleveland Clinic, Holy Cross / Memorial, and Montefiore. Their virtual tools are driving a differentiated engagement and experience, as well as driving care delivery usage patterns. They’re well positioned to benefit from their individual members flipping to MA plans. They’ve improved their margins over time, albeit very slowly. As they continue to scale this up, they could be your next Fortune 50 insurer.

Bear: They haven’t built anything different from any other insurer beyond a nice engagement tool, which clearly hasn’t helped them manage insurance costs any better given the losses they’ve sustained. And, every insurer has a functional app with provider search and video visits these days. They seem to be sustaining more losses as they scale, and their Admin Expense went up as a percent of premiums over the last year! They haven’t demonstrated they can manage risk as an insurer and there is no end in sight to the losses.

Give me the bull case all day, personally.

The SPACs:

I’m getting a bit tired of all the SPAC shenanigans at this point, which is unfortunate because as I was reminded on Twitter this week there are currently 58 healthcare focused SPACs still actively seeking a target. Can you imagine 58 more of these things? Yeesh.

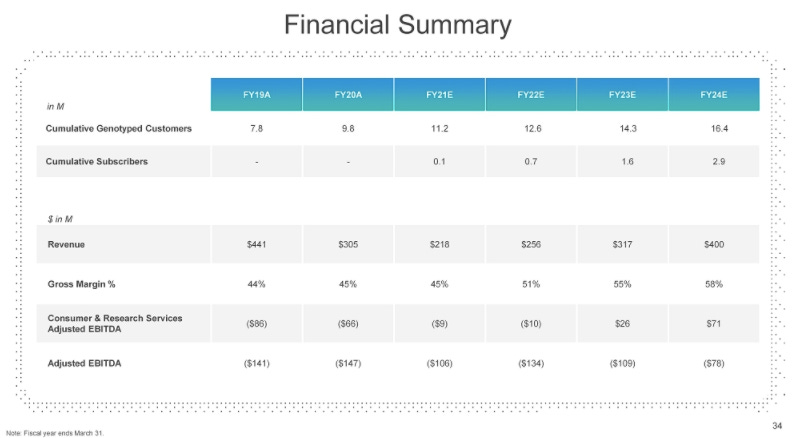

The 23andMe SPAC was officially announced this week. And while I want to like the company that has brought genetic screening to so many folks, I found the investor presentation (linked below) to be pretty confusing and unhelpful. I also generally struggle to comprehend how a company can be going public while providing this summary financial picture:

Let’s recap - revenue has dropped roughly 30% each of the last two years, going from $441 million in FY2019 to $218 million in FY 2021. Mind you, this was in the midst of a pandemic when the at-home testing market has exploded around 23andMe. It has also lost over $100 million in Adjusted EBITDA in each of the last three years. Meanwhile, over the next three years it’s growing revenue back to $400 million - still significantly lower than FY2019, and it projects it will lose $134 million, $109 million, and $76 million in Adjusted EBITDA each year. These are the financials of a company that is being taken public at a $3.5 billion valuation, up from a reported $2.5 billion valuation in 2019 and 2020)? Is this real life?

It appears that the story justifying the deal is that 23andMe is shifting away from the consumer business - where they’re slowing growth and focusing on profitability - and instead focusing on driving growth by becoming a drug development partner for big pharma, playing up the GSK partnership they signed back in 2018. 23andMe says as much in the investor presentation: “…it's worth pausing to think that, really, the 23andMe platform is now one of the cornerstones of the future pipeline of a company, GSK, with a market cap of $100 billion.” Which, ok - I understand that there is a lot of money in helping pharmaceutical companies manage their pipelines and bring drugs to market faster. So maybe this provides 23andMe with a huge long term growth opportunity that justifies the valuation. Which is all well and good, but it seems like a far cry from the consumer-oriented disruptor story.

23andMe doesn’t entirely appear to be giving up on the consumer business, as they “soft-launched” a consumer subscription product in October that currently has over 75k subscribers. The subscription costs $29/yr according to their website. But I’m scratching my head trying to understand what you’re subscribing to here? Apparently you get access to more reports about your health? But… doesn’t that sound a lot like the original product? Why does someone need an annual subscription for a set of reports? I’m befuddled. They expect this business to grow from 75k to 2.9 million subscribers over the next three years, which would amount to approximately 16% of revenue in FY2024. They make some passing remarks in the investor call about how they have the opportunity to “usher in a new era of a genetics-driven primary care”… which just feels really buzz wordy without any semblance of a plan here.

All-in-all this SPAC feels like a lifeboat for investors looking to get some return out of the $850+ million invested into the company by dumping it on the public markets. Link (investor deck).

Clover found itself in a bit of a kerfuffle this week with Hindenburg Research, a short-selling research firm. Hindenburg released a report on Clover centered around an undisclosed DOJ request for information on a number of topics related to Clover’s sales practices, if it’s paying for referrals, the Clover Ambassador program, and the Clover Assistant software. I was actually pretty impressed with Clover’s well-composed response to the questions raised by Hindenburg. They did a good job of responding, in particular knocking down some of the weaker issues raised in the Hindenburg Research. I found it interesting though that Clover’s response didn’t seem to touch on the DOJ’s requests into the Clover Ambassador program nor did it directly respond to whether they’re paying for member referrals. Those issues still seem unresolved to me here. Regardless of what materializes from this - and based off Clover’s response it sounds the SEC has already informed Clover that it is starting an investigation - it sure seems like a lot of smoke is emanating from Jersey City on this one. Link (Hindenburg Report). Link (Clover Response).

TalkSpace filed it’s S-4 for its SPAC. I can’t say I’ve looked through this one in depth given everything else going on this week, so check out my investor presentation analysis from a few weeks back if you’re interested. Link.

Other News:

Humana partnered with DispatchHealth to build a hospital at home program, first starting in Denver and Tacoma. They’ll expand services to Texas, Arizona, and Nevada later this year. Dispatch seems to be gaining some serious momentum. Link.

Folx, a virtual care startup focused on the LGBTQIA+ population, raised $25 million. Interesting to see the perspective from Bessemer in this article: ““At a high level, 2% of the population identify as transgender… At that math, when we looked at that, we were able to see a multibillion-dollar market opportunity not just to provide [hormone replacement therapy], but to provide a healthcare destination for this community.” It seems like we’re going to see a ton of investment crop up this year with a similar thesis - a healthcare destination for a specific slice of the population. Link.

MSK startup SWORD Health raised $25 million. Link.

Flywheel raised $15 million for its data management platform for clinical researchers. Link.

Plume, a virtual hormone therapy provider for the transgender community, raised $14 million. Link.

Casana raises $14 million to commercialize its toilet seat with sensors. Link.

Garner Health raised $12.5 million for its analytics platform to help get employees to use high quality / low cost providers. Link.

Bold raised $7 million for virtual exercise programs for seniors. Link.

Telemedico, a telehealth platform based in Europe, raised $6.6 million. Link.

Modern Health, a digital mental health startup, acquires another digital mental health startup, Kip. Link.

Anthem acquired the largest Medicare Advantage plan in Puerto Rico. Link.

Onduo has expanded from Type 2 diabetes to hypertension and mental health. Link.

UnitedHealth Group got a new CEO this week, with Sir Andrew Witty stepping into the role. Link.

Opinions:

In this weeks excursion into insane hospital billing, check out this NYTimes article from Sarah Kliff and Jessica Silver-Greenberg on how some hospitals are profiting off patients who get in car crashes. The article focuses on the Parkview Hospital system in Indiana, which has a history of trying to sidestep Medicaid and place liens on car accident settlements. The opening anecdote is tough to read - a patient was transported to the hospital after a car accident and showed her Medicaid insurance card. They chose not to bill Medicaid but rather put a lien on her accident settlement, so that the hospital could bill 5x the amount. One hospital in Washington reportedly made $10 million annually with this tactic. This stuff is just so infuriating. Link.

This is an interesting read in Health Affairs on suggestions for Medicaid to improve care. It looks at both types of new demonstrations and models as well as waivers and other investments. Link.

Here’s a fun look under the hood at how the US Digital Service is tying to modernize the CMS mainframe for Medicare claims processing. It’s eye opening some of the challenges they face with COBOL, like the issue with decimal points. Link.

Bessemer wrote about their 2021 predictions for healthcare. Worth checking out what one of the leading investors in the space is looking at - the commoditization of telehealth driving virtual care opportunities, a focus on underserved populations, backoffice automation, and more. Link.

This is a good read from LRVHealth’s Ellen Herlacher on how organizations can find success in moving more care delivery into the home - i.e. getting customer experience right, figuring out the financials, and execution. Link.

Here’s a piece in JAMA on provider consolidation and how the Biden administration might consider addressing some of the challenges associated with consolidation. It provides some interesting recommendations on how to address those challenges. Link.

Data:

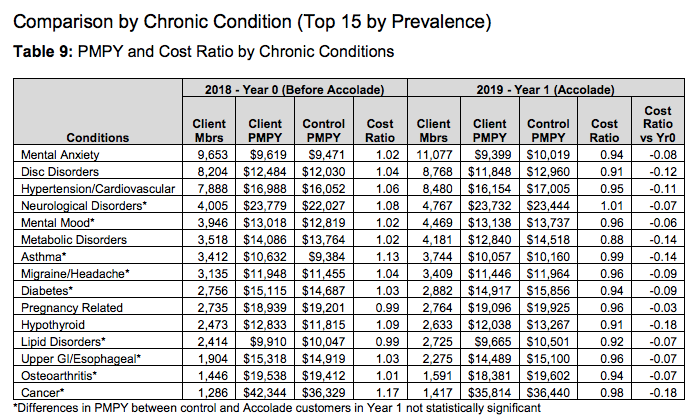

Accolade released an study conducted by Aon looking at how Accolade impacts costs with employer customers. Not surprisingly, the report looked at six employers where Accolade had a relative improvement on PEPM costs versus a control group each year. Interesting to see how Accolade impacts costs by service category, age band, comorbidities, and member costs. The chart below provides a nice summary of common chronic conditions and costs for the employers. Link.

This is an interesting report from the Urban Institute looking at how a Medicare buy-in for individuals ages 50 - 64 could potentially help reduce healthcare costs, essentially because with a buy-in more providers would be getting paid Medicare versus individual or commercial market rates. Link.

Minneapolis(!!!!) data analytics startup Carrot Health released a report on Medicare open enrollment results providing some interesting insights into factors that drove plan growth during the open enrollment period. Link.

Jobs:

Alula, a startup supporting patients through the oncology journey, is hiring a Sr Partnerships Manager. Link.

Devoted Health, a Medicare Advantage insurance startup, is hiring a Sales Strategy & Operations analyst. Link.

Iora Health, a Medicare Advantage primary care startup, is hiring a bunch of roles. Link.

Memora Health, a care delivery infrastructure startup, is hiring for care delivery product, ops, and engineering roles. Link.

Mount Sinai, a NYC-based health system, is hiring a Manager, At Home Services for its care delivery for patients at home. Link.

Panda Health, a digital health procurement marketplace for health systems, is hiring a Director of Category Growth. Link.

Redox, a healthcare integration platform and network, is hiring for a bunch of roles including sales and customer success. Link.

Ribbon Health, a startup building an API layer for provider data, is hiring a Enterprise Sales Lead for Digital Health. Link.

Rupa Health, a specialty lab portal for integrative medicine, is hiring a head of marketing and user operations. Link.

Tytocare, a consumer-focused remote monitoring startup, is hiring an account management role. Link.

That Oscar Health S1 summary was excellent! Thanks for putting this together Kevin.